Understanding the OAS Payment Schedule for 2026: What You Need to Know

Curious about the OAS payment schedule for 2026? While exact dates can vary, staying informed on the latest updates is key to effective planning. This article offers insight into potential timing based on historical trends and government announcements, ensuring you stay ahead.

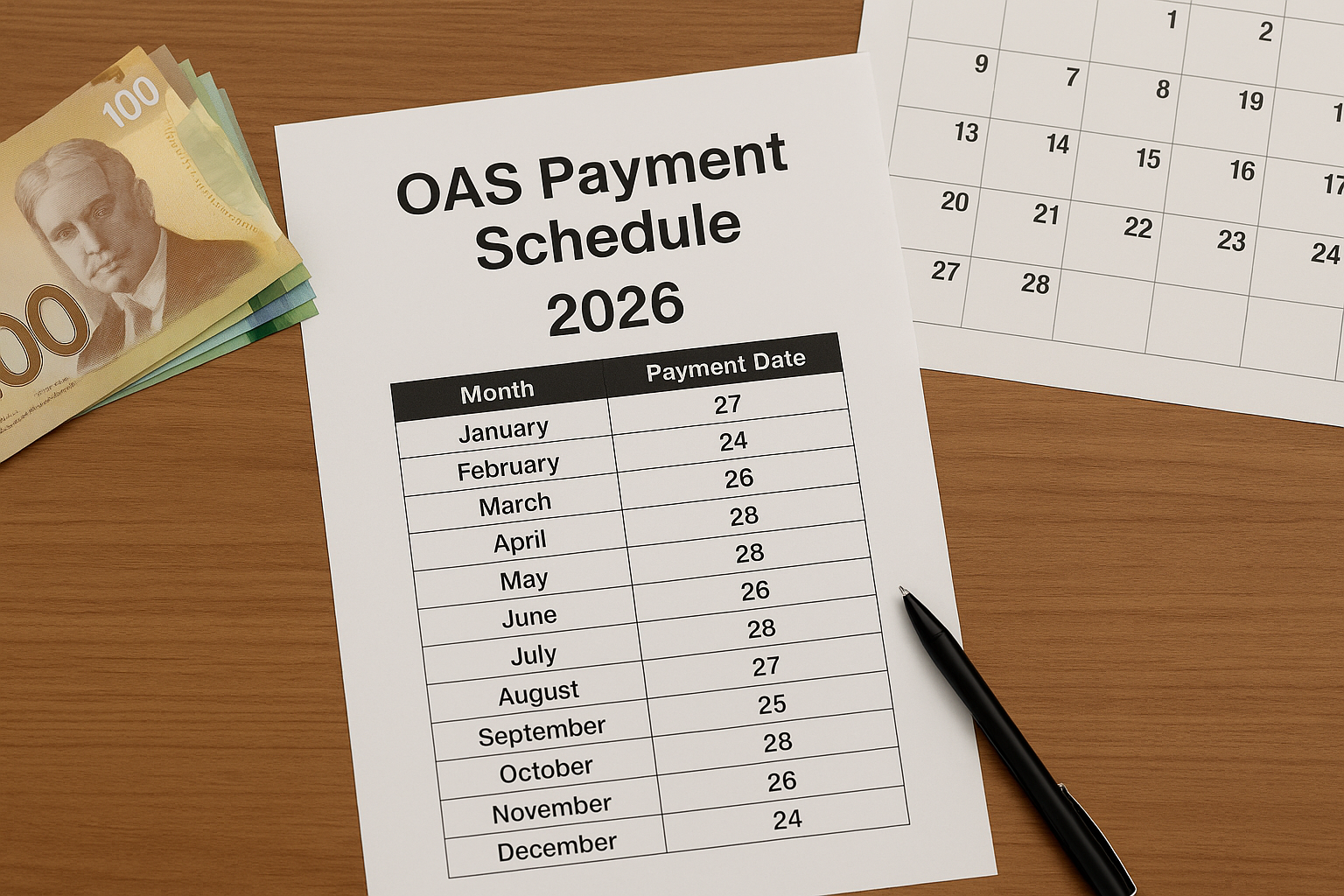

Understanding the OAS Payment Schedule for 2026

The Old Age Security (OAS) program is a cornerstone of Canada's public pension system, providing a source of income to seniors aged 65 and over. As we look towards 2026, many individuals are keen to understand how the OAS payment schedule will affect their financial planning. This article aims to provide a comprehensive look at what you can expect from OAS payments in 2026, addressing key questions and offering insights into the changes and what they mean for recipients.

What is OAS?

OAS is a government-administered pension plan that provides benefits to Canadian seniors, regardless of previous workforce participation. This program is funded by general tax revenues rather than individual contributions, distinguishing it from the Canada Pension Plan (CPP). Eligibility begins at age 65, but benefits can be deferred for up to five years, leading to increased monthly payments.

Key Changes to the OAS Payment Schedule in 2026

In 2026, several key changes are planned for the OAS payment schedule, reflecting government policy shifts and adjustments for inflation. Understanding these changes is crucial for financial planning:

- Quarterly Indexing: OAS payments are indexed quarterly to keep pace with inflation. In 2026, recipients will see adjustments every January, April, July, and October, ensuring that payments maintain their purchasing power over time.

- Increased Payment Rates: The basic OAS pension rates are set to increase. While the exact figures are subject to inflation projections, the government has committed to ensuring that benefits continue to provide adequate support to seniors.

- Clawback Thresholds: High-income seniors are subject to the OAS clawback, officially called the OAS Recovery Tax. The threshold for this tax will also be adjusted for inflation in 2026, affecting how much high-income seniors can keep, tax-free.

How OAS Payments are Calculated

The amount of OAS you receive is based on your residence in Canada. To qualify for the full OAS pension, you must have lived in Canada for at least 40 years after turning 18. If you have lived in Canada for fewer years, you may still qualify for a partial pension if you have lived in Canada for at least 10 years after the age of 18.

Impact of Deferring OAS Payments

Deferring OAS payments can significantly impact the amount you receive. For each month you defer, up to a total of 60 months, your OAS pension increases by 0.6% per month, or 7.2% annually. This means if you defer for the full five years, your monthly OAS payment could increase by 36% when you start receiving it at age 70.

Who is Affected by OAS Clawback?

The OAS clawback affects seniors with a net income exceeding the minimum threshold, which for 2026 is expected to be around $85,000. The clawback is calculated at a rate of 15% on every dollar above this threshold, effectively reducing the OAS benefit for higher-income earners up to the potential full clawback amount.

Planning Your Retirement with OAS

When planning for retirement, it's crucial to integrate OAS into your broader financial strategy. Consider the following tips:

- Understand Your Income Sources: Take stock of all potential income sources, including CPP, private pensions, savings, and investments, to manage your tax situation effectively.

- Consider Deferring Payments: If you have other income sources and can afford to defer, higher OAS payments may better support your retirement needs over time.

- Monitor Tax Implications: Be aware of how OAS payments impact your tax bracket, especially if you are close to the clawback threshold.

Real-World Example of OAS in Action

Consider Jane, a 66-year-old retiree who opted to defer her OAS for a year. By doing so, she increased her monthly payments by 7.2%, providing her with a greater long-term income to manage rising living costs. Jane combines her OAS with CPP and personal savings, giving her a balanced and reliable income stream in retirement.

Where to Get More Information

For those seeking more information on the OAS payment schedule for 2026, several resources are available. The Government of Canada's public pensions site offers detailed insights and the TD Bank Retirement Planning resources also provide tools and advice to help plan effectively.

https://www.canada.ca/en/services/benefits/calendar.html

https://www.canada.ca/en/services/benefits/publicpensions/old-age-security/while-receiving.html

https://www.canada.ca/en/services/benefits/publicpensions/old-age-security.html

https://www.canada.ca/en/employment-social-development/services/my-account.html

https://www.canada.ca/en/public-services-procurement/services/payments-to-from-government/direct-deposit.html

https://www.canada.ca/en/public-services-procurement/services/payments-to-from-government/direct-deposit/help-centre.html